Wider Deficits, Stronger Bitcoin: Connecting US Presidential Candidates

No matter the outcome of the U.S. Presidential election, one thing is inevitable: wider deficits. Both candidates have shown little interest in fiscal restraint, setting the stage for a significant increase in government spending relative to sluggish economic growth. Harris and Trump may seem to be at opposite ends of the political spectrum, but when it comes to fiscal policy, they are simply two sides of the same coin. A wider deficit and lower interest rates will likely weaken the U.S. dollar, driving investors to seek alternatives like Bitcoin.

Geopolitical conflict in the Middle East may initially weigh on crypto markets due to heightened risk aversion and short-term volatility. However, history shows that Bitcoin thrives in times of uncertainty. Bitcoin’s resilience as a decentralized, borderless asset has shone in past crises—and this time should be no different.

Both US Presidential Candidates Committed to Wider Deficit

Much is made about increasing political polarization in the US, and for good reason. The Vanderbilt Unity Index reveals the increasing disunity, as seen on social media platforms. However, as Lyn Alden points out in her latest newsletter, despite the differences between US Presidential candidates Kamala Harris and Donald Trump, they are closely aligned on a few key points. In years past, deficits and the national debt were major election issues, but that is no longer the case.

Source: Vanderbilt Unity Index reveals the increasing disunity

The Republican Party is historically the party of fiscal conservatism, but ahead of the elections, one of the key promises is to "fight for and protect social security and medicare with no cuts, including no changes to the retirement age.” This shift illustrates that neither side is focused on deficit reduction as a priority. Democrats and Republicans may appear to represent opposite ideologies, but on this issue, they are two sides of the same coin—both committed to spending, regardless of long-term debt implications.

Wider Deficits Despite Low Unemployment

The disinterest in deficits is abundantly clear when examining the relationship between the deficit and unemployment.

Typically, the deficit widens sharply during periods of high unemployment (recessions) and normalizes thereafter. However, after ballooning to an all-time record during COVID, the deficit has remained wide ever since, despite low unemployment. As of 2024, the deficit is widening again, and we have not yet entered a recession. Like a dam with ever-widening cracks, the U.S. deficit is straining against pressure, with no relief in sight. I encourage you to read Lyn Alden latest piece which argues why this pressure will continue to build.

US Credit Risk on the Rise

Widening deficits suggest far bigger risks in US debt than ever before. If governments from both major political parties cannot address fiscal sustainability, what hope is there to contain debt levels? Higher inflation and a weaker dollar are essentially the only viable tools for the US government. Debt must be monetized, and foreign holders must take a currency haircut.

In addition to inflation and currency risks, there is growing concern that foreign powers and investors will increasingly seek alternatives to US debt as a reserve asset. The rise of China, the proliferation of non-USD trade agreements, and the US decision to freeze Russian reserve assets all point towards this shift. This could accelerate a reassessment of global reserves.

Gold's breakout vs Real Rates Speaks of Regime Change

Gold's breakout in the face of rising real interest rates points to a broader regime change in global monetary conditions. While real rates remain valuable in many contexts, they no longer provide a full picture of the US financial system’s credibility.

Holding U.S. debt in this environment feels like holding onto a rope that is fraying at both ends. Investors and sovereign nations must now consider a more diversified mix of reserve assets due to potential risks, such as the seizure or freezing of assets. This shift favors both gold and bitcoin, two store-of-value assets with no counterparty risk, which could play a central role in the future financial system.

USD Reserve Status Intact and Supported by Crypto

It is important to note that concerns about the USD and the US financial system do not imply that the dollar's status as the primary global reserve currency will be unseated anytime soon.

Data from Visa, Brevan Howard and Castle Island ventures provide key insights in this regard:

Stablecoins are dominated by the USD far more than the USD dominates foreign exchange reserves, international debt or SWIFT payments. This suggests that despite the challenges facing the USD, it remains highly appealing for non-US participants to gain access to the dollar network.

Source: Visa, Brevan Howard, Castle Island Ventures

Crypto through stablecoins makes USDs far more accessible to millions. This crypto trend supports USD adoption globally, reinforcing its reserve currency status.

The survey also reveals that stablecoins are increasingly used for non-trading activity, bolstering our argument that crypto is not merely a tool for speculation.

Source: Visa, Brevan Howard, Castle Island Ventures

As stablecoin adoption grows (potentially supported by US stablecoin regulation), we expect stablecoins to benefit from the broader trend of crypto adoption, supporting the dollar’s role as the primary reserve currency. Additionally, crypto assets themselves will benefit from stablecoin adoption. Once users have stablecoin wallets, it will be far easier to onboard them into BTC or ETH. I.E. We envisage a world where the USD remains prominent in the global monetary order, and BTC & ETH play a far bigger role than they do today.

Falling Rates and Widening Deficit - Cocktail for the DXY

While real rates have risen, markets are forward-looking. Real interest rates are expected to remain negative for many years due to the enormous debt stock that requires monetization. The Fed has already cut interest rates by 50bps with equity markets near record highs—an unusual combination.

Stanley Druckenmiller hopes that the "Fed is not trapped by forward guidance the way they were in 2021. GDP is above trend, corporate profits are strong, equities' all-time high, credit tight and gold at new highs. Where is the restriction?"

This combination of rate cuts and wide deficits is extremely bearish for the USD in our view. If the US economy does enter a weaker growth patch, we expect the deficit to widen further, which would put even more downward pressure on the dollar.

Conflict Poses Further Deficit Risks & Empowers the Oppressed

In the short-term the market is worried about risk appetite due to Middle East conflict fears, which have weighed on bitcoin. This temporary volatility likely stems from a misunderstanding of Bitcoin’s role as a long-term store of value. Yes, we must accept that in the short-term bitcoin acts like a risk asset. But in the medium to longer term, bitcoin benefits from conflict.

History has shown that in war-torn countries, decentralized financial technology becomes a lifeline drowning in chaos. The Russia-Ukraine war offers numerous examples of both sides using crypto for its censorship resistance, store of value and portable characteristics.

Further conflict draws in global powers, maintains defense spending and widens the deficit. While recession fears might temporarily affect risk appetite, markets will likely look beyond this to the more significant implications: lower rates, more liquidity, wider deficits, and increasing crypto use cases.

Coincidently, Blackrock recently published this research which shows bitcoin's outperformance 60 days post major geopolitical events in the past few years

Source: BlackRock

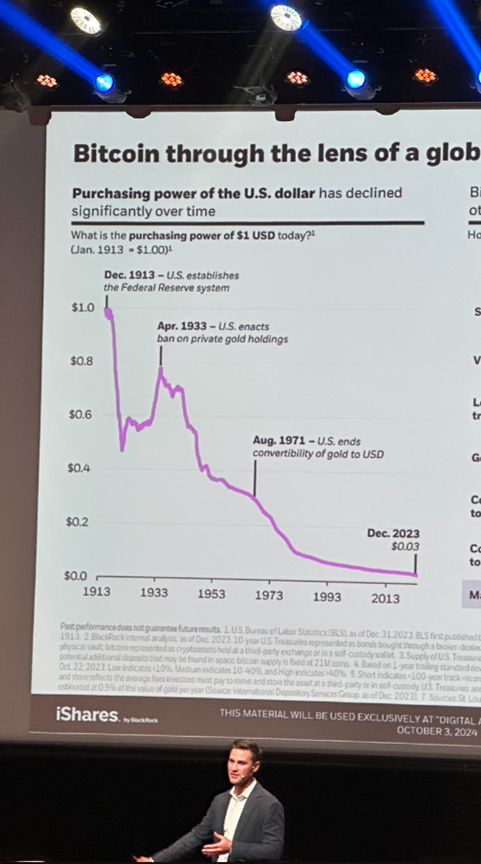

On the topic of BlackRock, its employees are straight-up talking to clients about dollar debasement. This raises awareness of the structural problems with the existing monetary system, opening the eyes of millions of capital allocators, with billions of dollar, to bitcoin.

Source: iShares

Sustained DXY Decline Below 100 Expected

Bitcoin has been consolidating over the past six months, underperforming while the dollar weakening trend has already started. We believe this creates a significant opportunity for catch-up, particularly as the pressure from Mt. Gox supply unlocks and government sales in the US and DE has largely subsided.

We continue to expect a downdraft below 100 on the DXY over the coming quarters, which could provide a major boost to Bitcoin and crypto markets. The upcoming elections are also key. While Trump presents a potential opportunity for crypto with promises of clearer legislation, a Harris presidency could still support the broader macro environment into 2025. Regardless of the winner, deficits are expected to remain wide.

Historically, the post-election period has been positive for Bitcoin, and we believe political certainty may provide the confidence to break out of this sideways market. Think of Bitcoin’s recent consolidation as the calm before the storm, a period of stillness before the next surge.