PayPal reflects crypto’s powerful potential & inevitable impact

PayPal's foray into the world of stablecoins is a major step in the integration between crypto and traditional financial markets. This move not only underscores the potential of crypto but also hints at a possible pendulum shift in the landscape of US crypto regulation that we have been warning of. While the crypto market experienced a period of relative calm in June with falling volatility, it's crucial to examine the broader context and long-term trends that define Bitcoin's remarkable performance and its unique characteristics as an asset class. Bitcoin remains the asset allocation panacea. It might take higher prices until some are willing to admit as much.

CONCLUSIONS

Bitcoin stands alone vs traditional asset class peers

Bitcoin has decoupled vs equities

Bitcoin is the asset allocation panacea

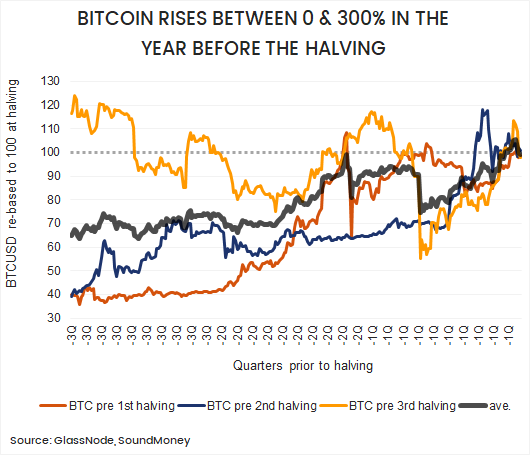

Price and reputational risks are easing ahead of 2024 halving

Stronger USD and Binance present price risks in H2 2023

PayPal’s PYUSD is a major vote of confidence for technology

PayPal could signal a pendulum shift towards more constructive US regulation

Market lull with FALLING VOLATILITY

Price went into a relative lull In July after the spot bitcoin ETF applications squeezed price temporarily above $30K in June. 30 day realised volatility has fallen to levels comparable with 2019 and 2020 reflecting the quiet market conditions. These quieter conditions provide a great opportunity to pull back the lense and provide long-term context of bitcoin's impressive performance and constructive cyclical outlook.

asset class characteristics stand alone

Following the bear market, BTC has returned 85% since the November 2022 low and 27% in the past year, close to the 5-year annualised returns of 31%. No asset class has kept pace during this period despite the crypto bear markets in 2018 and 2022

BTC returns since the peak of the 2017 bull market also far surpass any comparable asset class. Bitcoin fell 80% between Dec 2017 and Dec 2018 and 77% between Nov '21 and Nov '22, making the outperformance during this period remarkable.

This outcome confirms that volatility does not matter if one has a long enough time horizon

Bitcoin HAS DECOUPLED FROM EQUITIES

One of the most striking and conclusive changes in 2023 is the shift in the correlation between Bitcoin and traditional stock market indices such as the S&P 500 and the NASDAQ from positive to negative.

The negative correlation statistically confirms what we should have known already. Bitcoin is a fundamentally different asset class from equity market. Yes, both assets are effectively by central bank liquidity. But unlike equities, Bitcoin is less influenced by the economy and it has no dividend payments, income, or yields. Instead, bitcoin functions as a pure store of value and an alternative monetary system.

Viewing bitcoin as high beta equity is overly simplistic and hides its powerful value

Why resist the Asset Allocation Panacea?

The combination of uncorrelated and outsized returns is the asset allocation panacea. Historically, a 1% allocation to bitcoin, with monthly rebalancing, boosted annualised returns of a balanced (60% S&P500, 40% Barclays Aggregate) by 3% with minimal impact on drawdowns and volatility.

The cold hard numbers reveal that crypto allocation remains a no-brainer

Observers may ask, what is restraining allocation? A recent family office survey from Campden Wealth indicated the usual obstacles; volatility, regulatory uncertainty, limited understanding, and the maturation of the crypto market.

I find these obstacles rather exciting, as they are gradually being addressed. Over time, the market is becoming more mature, and various jurisdictions (like Hong Kong, Dubai and Singapore) are actively developing regulatory frameworks for the crypto industry. Understanding of decentralised financial technology and the challenges posed by our centralised status quo also continues to advance. But there is another factor that is very unlikely to show up on investor survey's…

PRICE remains NB & REPUTATIONAL RISK MATTERS

Experience tells me that dramatic price increases remain a massive unrecognized adoption driver. Investors won’t admit it, but often purchase because price has increased. When bitcoin's price returns to its previous all-time-highs many people are awakened from their slumber and think "I said was going to make that allocation" and so they finally take action. Somehow investing in crypto feels safer with bear market losses in the past. Rather than stick their heads out at low prices, many would prefer to invest alongside the crowd with compelling narratives emerging in mainstream media. BlackRock would be a nice crowd to invest alongside.

Regular readers do not fall into this category but will likely use this dynamic to position strategically, ahead of the crowd

The halving remains a key cyclical indicator of the transition from an early bull-market towards a frothier bull-market. We are now less than 3 quarters away from the next halving, when bitcoin supply growth will be cut in half. Historically, bitcoin price has moved up to sideways in the year leading up to the halving (310% pre 1st halving, 132% pre 2nd halving and 7% pre 3rd halving).

Bitcoin tends to experience more aggressive gains in the year after the halving (6562% post 1st halving, 300% post 2nd halving and 542% post 3rd halving).

From a purely cyclical perspective, the price outlook over the next 3 quarters is moderately constructive (in bitcoin terms). This is the time for suitable positioning ahead of the more aggressive price gains that tend to take place in the following year.

STRONGER DOLLAR & Binance present risks

In terms of risks on the horizon, we are watching the USD and Binance developments closely. A weaker dollar supported risk asset gains in May and June, but the DXY has gathered some strength at lower prices. Rising yields, bond weakness and dollar strength are factors to keep in mind in the coming quarter because they could restrain risk appetite. I have no edge to provide on the inner workings of Binance and the SEC case but BNB price action suggests to me that there is further pain and potentially bad news in the pipeline. A negative reaction from bitcoin and ethereum to the USD or Binance would likely present great buying opportunities. We remain constructive on the market over the next 12-18 months.

US REGULATORY TRAJECTORY SHIFTING POSITIVELY?

On the news front, PayPal announced this week that it will launch a USD stablecoin, which is a big vote of confidence for crypto technology and suggests the regulatory trajectory in the US might be shifting. The previous big PayPal crypto announcement on October 21, 2020 PayPal that customers to buy, hold, and sell cryptocurrencies directly from their PayPal accounts marked a significant step towards mainstream adoption of cryptocurrencies by a major financial platform. This week’s announcement could mark a similar shift because it could bring millions of people into DeFi with its stablecoin. Paypal has ~400 million active users, and holds about $1 billion in BTC & ETH for them. With a USD stablecoin, users will now be able to utilise PayPal deposits outside of the PayPal ecosystem.

It is unclear whether PayPal has inside knowledge regarding US regulations. Perhaps they are just pushing the boat out in the expectation that Congress will pass the Stablecoin Bill at some point? We have warned numerous times that the regulatory trajectory would eventually turn positive again. We are also of the view that stablecoin adoption, like bitcoin, is inevitable and that US Congress will eventually realise that the proliferation of USD stablecoins across the globe is a wonderful tool to maintain USD global reserve currency status at a time when de-dollarisation has become a theme.

Readers are encouraged to listen to this interview with Democrat Representative Ritchie Torres for further insights on the regulatory landscape and read this article from Austin Campbell for further insights on PYUSD.

Continuing on the US regulation theme, the Ripple case in US courts started to provide some clarity on the application of securities law for crypto tokens. Most importantly, the ruling creates the precedent that not all crypto tokens are securities. The SEC’s regulation by enforcement action approach was predicated on the assumption that all non-crypto assets were securities so contradictory evidence is impactful. The judgement is not 110% conclusive as the case will likely go to appeal but we have seen major US exchanges list XRP again and Coinbase shares rose strongly on the news, reflecting the reduced risk to crypto exchanges. This ruling is encouraging for broader crypto markets and non-bitcoin assets in particular.

Adopt and innovate or be left behind

The simple reality is that crypto presents a technological upgrade on traditional finance. Sure, it is new, innovative and imperfect, but a truly scarce digital token like bitcoin is profound. As is the ability to open a USD bank account anywhere in the world and execute 24/7 peer to peer USD payments on stablecoin rails. The incumbents have a choice to adopt and innovate, like PayPal, or be left behind. The same goes for regulators who face competition abroad. We continue to expect a bitcoin spot ETF in the US over the coming year and a continued shift towards more constructive regulation that will pave the wave for further adoption and integration with the traditional financial system. Crypto prices might have been in a relative lull in June but this will not last over the coming 12-24 months as we head towards bitcoin’s halving.